Retirement Plans for the Millennial Solopreneur

Navigating retirement savings as a millennial solopreneur can be difficult. You are building your business while also wanting to be sure you don’t underfund your retirement.

You also may be unsure how to invest your money. Do your parents use an advisor already? Do you like them? What about a friend?

Or are you more of DIY investor that would work well with my firm, Bird Spring Financial.

And then how do you actually fund the plan?

This article will deal with generalities as they exist in tax year 2024 and is meant to give you an overview. Before doing anything, an analysis should be done by a competent professional. I offer free introductory meetings. Schedule your meeting today.

Personal Retirement Choices

Before considering whether to open a business retirement plan you should consider the options available to you without doing anything with your business. IRA (Traditional or Roth) and an HSA are the two main ones.

Individual Retirement Account (IRA)

A Roth IRA offers tax-free withdrawals in retirement. The biggest plus is there is no RMD requirement (RMD’s are required minimum distributions the IRS imposes on your account to help it stop growing and ensure it is being used for retirement). Meanwhile, the Traditional IRA provides an upfront tax deduction, suitable for those anticipating a lower tax bracket in retirement and less interested in the other Roth features. And if you don’t have access to a retirement plan anywhere else you are eligible to fully deduct the traditional IRA contribution regardless of income.

You can contribute to this for 2023 and 2024 up until 4/15/2024.

Roth Conversion

As you start your business you will likely be in a much lower income tax bracket. If you have the means to do it, you could convert an old 401(k) to a Roth IRA. While you wouldn’t be saving in the traditional sense, you would be reducing your taxes in the future by paying them today while you are in a lower bracket.

Health Savings Account (HSA)

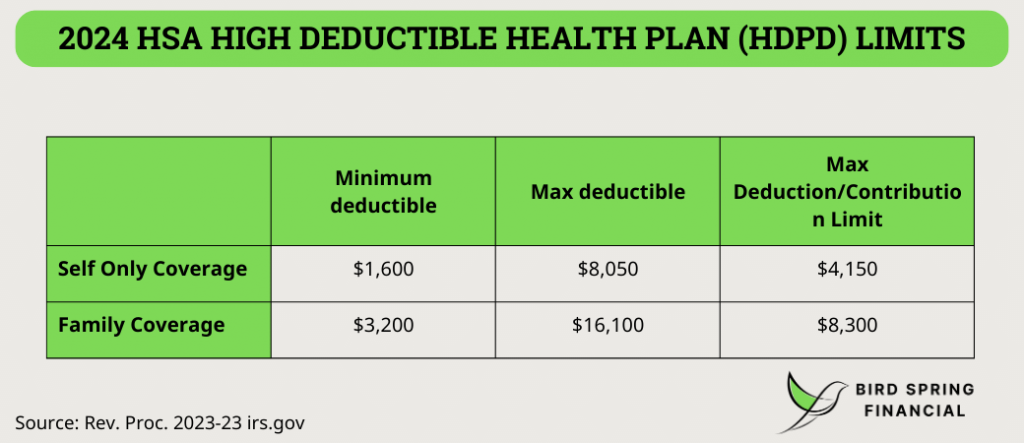

As a solopreneur you have more control over your health insurance options so you can opt for an HSA eligible plan. A HSA is a health savings account. Funding the HSA gives you an income tax deduction, the assets in the HSA can be invested to grow tax deferred, and then any expense you have while account is open can be withdrawn tax free. Say you have a surgery in 2024, you can withdraw that money from your investments tax free in 2060 (assuming tax law stays as it is now). These are eligible to those with a “high deductible health plan” and are best if you can afford the higher out of pocket maxes.

And as a millennial you may not have any major healthcare expenses so an HSA eligible plan may be perfect. You receive an income tax deduction up to your contribution in the HSA.

Your insurance won’t cover as much so you may have to pay up to the out-of-pocket maximum, generally around $8,000 if something truly terrible happened. However, the plan still provides you with discounted rates and thanks to the No Surprises Act emergency services are required to be covered. I had an ER visit this year with my HSA eligible plan and only ended up paying around $2,500. My insurance applied discounted rates from an initial bill of $20,000, balance billing is not allowed, and I made out better than expected. While that is still a lot of money, the income tax deduction of a $7,750 family HSA contribution in 2023 can result in savings of 22% if you are in the 22% marginal tax bracket! So, I can receive a tax discount of 22% of $7,750 or $1,705 that helps cover the unexpected cost. And I don’t expect to be in the ER each year. If you are in the top bracket in 2023, the ordinary income tax savings total $2,867.50.

You can contribute to this for 2023 and 2024 up until 4/15/2024.

Taxable Brokerage Account

You can also contribute open a brokerage account and use it to save for retirement and major purchases. There aren’t any special tax advantages to this however you may be surprised by how large the 0% capital gains rate. For 2024 a single filer could have up to $61,625 in income while being subject to no capital gains taxes. This bracket is a great spot to implement capital gains harvesting to increase your taxable basis in your investments.

While you won’t be in this bracket long if your business is growing significantly, you can use it during transition years or down years to better avoid taxes in the long run (tax avoidance is legal, tax evasion is not!).

Business Retirement Accounts

Now you can’t contribute all that much to the personal investment vehicles mentioned above. If you need to contribute over $22,300 in 2024 you would have to turn to taxable brokerage accounts. Which still can be useful, especially if your income falls in the 0% long term capital gains bracket.

There are business-specific options like the SEP-IRA, Solo 401(k), and SIMPLE IRA plan.

- SEP-IRA: A great choice for those with variable income, as contributions can vary each year. Simpler than a Solo 401(k) to manage but lower contribution limits at smaller income levels. More custodian options. Can contribute for 2023 up until your businesses tax return due date including any extensions. Easier to do this with a SEP than a Solo 401(k).

- Solo 401(k): Allows for higher contribution limits than a SEP-IRA. Additional tax filing required for accounts over $250,000. Catch-up contribution allowed for those over 50. Loan features. Can contribute for 2023 up until your businesses tax return due date including any extensions.

- SIMPLE IRA: Generally, not recommended for solopreneurs. This plan works best with employees.

Now how do you decide between the SEP-IRA and Solo 401(k)? They are actually equivalent from a tax standpoint if you make enough to maximize your contribution (unless you are over 50, then the 401(k) allows you an extra catch-up contribution). However, if you make less, the needle nudges more towards the Solo 401(k) because you are allowed to make elective deferrals just like you could to a normal 401(k) up to $23,000 in 2024 of 100%. Beyond that you can contribute 25% of your compensation up until the max. With the SEP, you are always limited by 25% of compensation and this may cause some complexities with payroll planning and S Corps as you are incentivized to increase your W2 earnings beyond what you and your tax person may consider reasonable. One benefit to the SEP-IRA is you are not required to file Form 5500-EZ like with a one-participant 401(k) with over $250,000 in assets.

Defined Benefit Plans for Maximum Retirement Savings

For millennials experiencing business success and reluctant to reinvest all profits in the business, the defined benefit plan provides a serious alternative with much higher contribution limits. This plan acts as a personalized pension, offering a fixed benefit based on factors like income and years of service. It’s a strategic move for long-term financial stability.

Implementation Insights

Implementing a defined benefit plan requires a thoughtful approach:

- Actuarial Analysis: An actuary will calculate your ideal contribution for the desired retirement outcome, emphasizing financial prudence over playfulness.

- Plan Documentation: Work with a professional to create a formal plan document, ensuring clarity and compliance.

- Annual Reviews: Your actuary will work with you on ensuring the plan is adequately funded.

- Cost: Expect to pay $4,000 or more to create this plan.

- Max Contribution: $275,000 in 2024 and determined by actuarial assumptions.

As you can see, you can contribute much more to a defined benefit plan but the cost and complexity will keep most people away.

Another Option — Deferred Compensation

Shohei Ohtani was recently in the news because it’s believed that his salary will be deferred with a Non-Qualified Deferred Compensation Plan (NQDC). This is great for athletes, highly compensated executives, and those that expect a significant reduction in earnings later in their working careers because you can defer your income to a later point where you will be in a lower tax bracket. And potentially avoid state income tax.

There are disadvantages such as bankruptcy protection and limited access to the money you defer.

Fidelity has a good article however you should always work with a professional who specializes in this area Nonqualified Deferred Compensation Plans (NQDCs) | Fidelity Investments.

Accessing your retirement account

Millennials have major life choices to plan for like buying a house, can consider early withdrawals from retirement accounts for a home down payment. IRAs offer penalty-free early withdrawals for home downpayments up to $10,000 however 401(k)’s do not. You can rollover from a 401(k) to an IRA before withdrawing. And there are other exceptions for life milestones like birth expenses, domestic abuse, medical, and more. The IRS publishes a list here for both 401(k)’s and IRA’s.

And sometimes paying the penalty isn’t a bad idea, you will have already benefitted from tax deferral on the growth and 10% penalty can simply be paid due to your fortunate financial position.

Future Financial Freedom for Millennials

This article was meant to give you a great starting point in understanding retirement investment options. Tailor your retirement strategy to your unique circumstances, and always consult with a financial advisor for personalized advice. Saving for retirement is a tradeoff and you can work with a financial planner like me to assist you in deciding how much to save and how much to use today. I offer free introductory meetings where we can see if we are a fit for working together.